The $7.5M Squeeze: How Tariffs and FX Are Hitting Cross-Border CFOs at the Same Time

A weaker dollar, new tariffs, and Fed uncertainty are converging at the worst possible time for companies with cross-border operations. The math on a $50M annual spend is brutal.

Jeff Forkan

March 17, 2026

Three Problems Hitting at Once

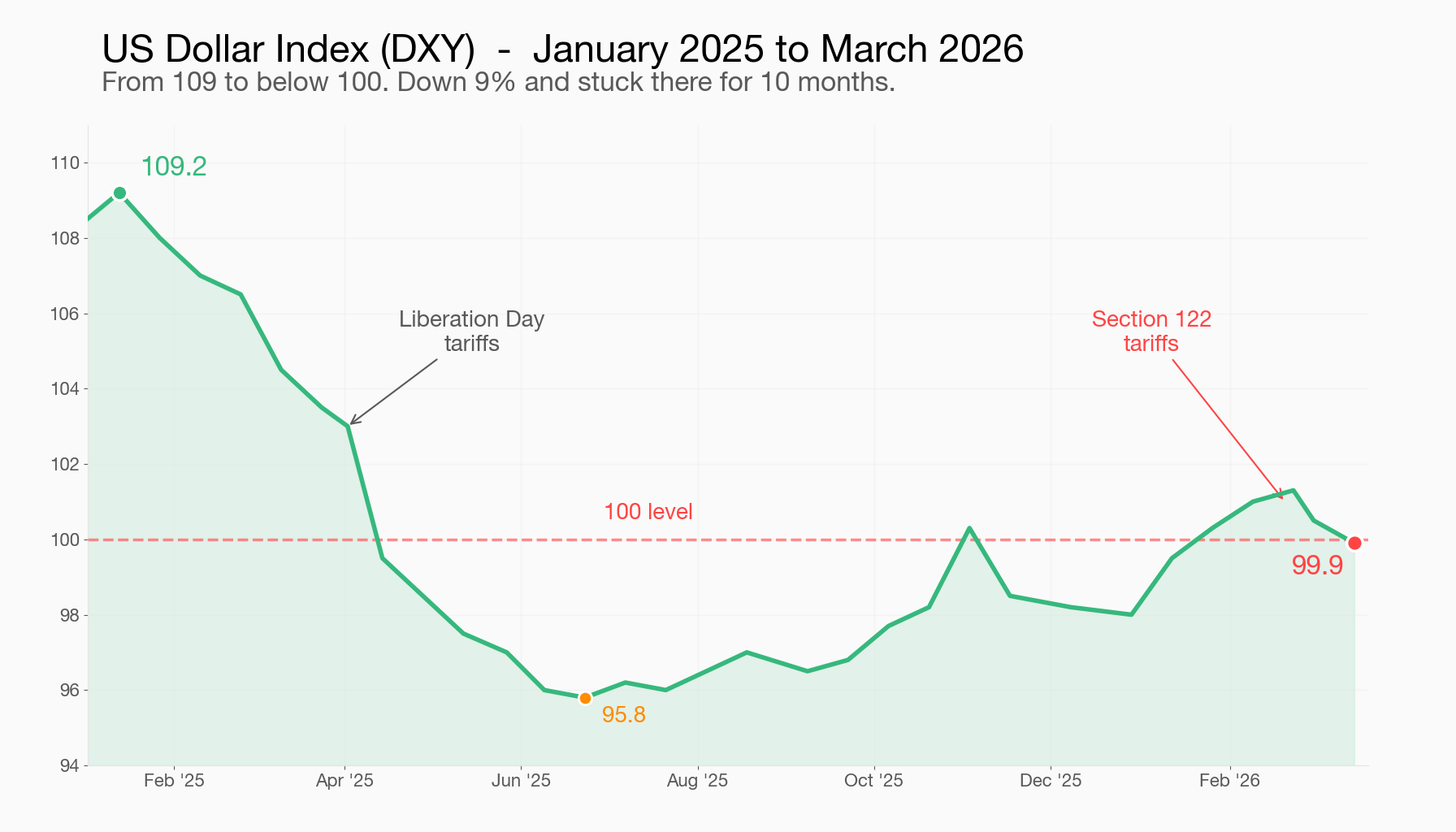

The dollar slipped back below 100 on the DXY index this week after briefly climbing above it in January. New Section 122 tariffs are adding 10% to imports. And the Fed announces its latest rate decision on March 19 with no clear signal on cuts.

If you’re running cross-border operations, any one of these changes your cost structure. All three at the same time? That’s a margin crisis most finance teams aren’t set up to see coming, let alone respond to.

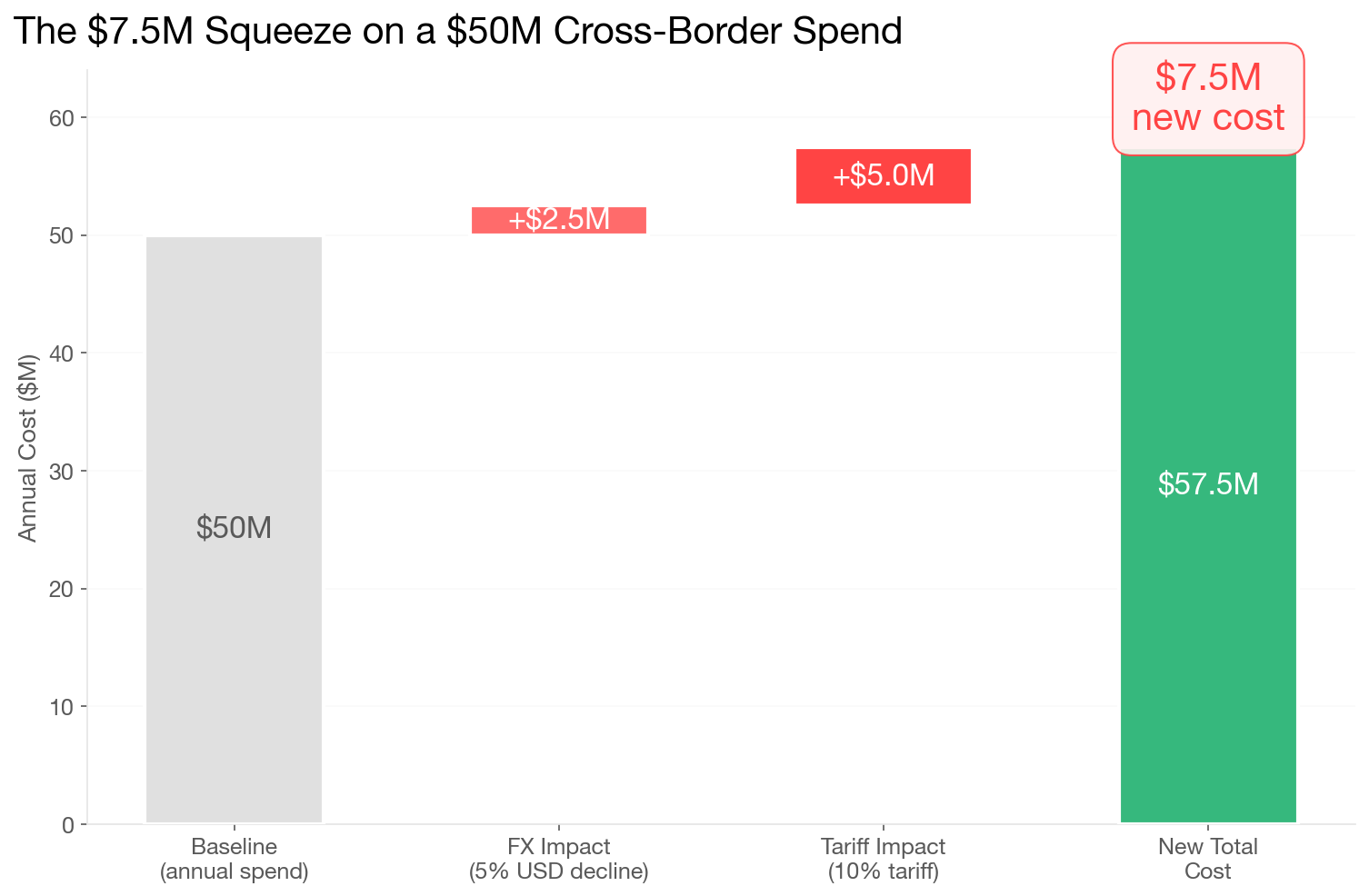

The Math on a $50M Cross-Border Spend

Let’s make this concrete. Take a mid-market company spending $50M annually across currencies: paying engineers in Tel Aviv, vendors in London, manufacturing partners in Tokyo.

A 5% dollar move against your expense currencies adds $2.5M in cost. The dollar is down 9% from its January 2025 peak of 109 and has been stuck below 100 for most of the past 10 months. That’s not hypothetical.

A 10% tariff on imported goods and services adds another $5M. The Section 122 tariff signed on February 20 applies broadly, with plans to raise it to 15%.

Both at the same time? That’s $7.5M in new cost that didn’t exist six months ago. For a company running 15-20% gross margins, that’s the difference between a profitable quarter and a board conversation about cash runway.

The CFOs getting hurt aren’t the ones who made bad decisions. They’re the ones who made no decision. They didn’t hedge because hedging seemed optional when the dollar was strong and tariffs were at zero.

Why this time is different

Currency swings and trade policy changes happen all the time. What makes right now unusual is that they’re all moving in the same direction, fast.

The dollar is weakening for the wrong reasons

Normally, tariffs strengthen the imposing country’s currency. That’s what happened initially. But the market has flipped. Higher tariffs are now being read as a drag on US growth, not a source of strength. The dollar dropped after the latest tariff announcements, which is the opposite of what the textbook says should happen.

So companies are getting hit on both sides. Tariffs make imports more expensive and the weaker dollar makes foreign-currency costs higher. There’s no natural offset.

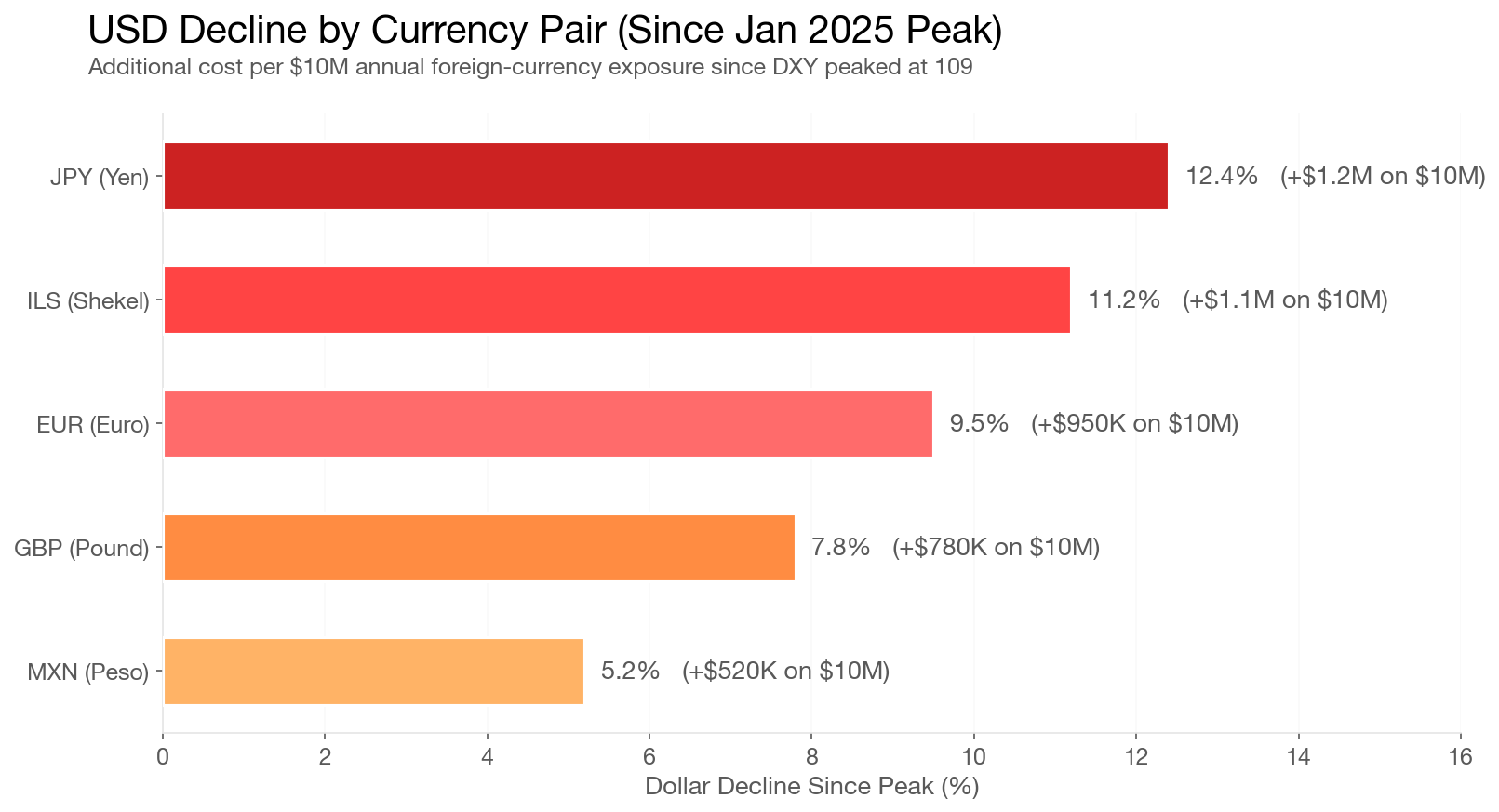

The yen at 159

The yen has weakened to 159 against the dollar, losing nearly 4% in a single month. If you’re paying Japanese suppliers or running an R&D office in Tokyo, those costs just jumped.

For a company paying $10M/year to Japanese suppliers, a 4% yen move in a single month is a $400K surprise. That compounds quarter over quarter.

The Fed is frozen

Markets are pricing in one rate cut this year, maybe, and not before December. Oil is elevated from the Iran conflict. Tariffs are adding inflation pressure. The Fed has no room to ease. Borrowing costs stay high and there’s no relief valve for companies trying to finance their way through tighter margins.

What the CFOs who aren’t panicking have in common

They can see their exposure in real time

They know what they owe in every currency, across every entity and bank account, right now. Not in a spreadsheet someone updates on Monday. Not in a report that’s stale before it hits the CFO’s desk.

This sounds basic. It’s not. Most mid-market companies discover their actual FX exposure during the quarterly close, weeks after the damage is done.

They’ve automated the hedging decision

Instead of debating hedges in treasury committee meetings, they’ve set thresholds. EUR/USD moves past a band, a hedge executes. Yen weakens past 160, forward contracts kick in.

The hardest part of FX management isn’t the instruments. It’s the timing. Nobody wants to be the person who hedged too early or too late. Automation takes that off the table.

They model the worst case before it happens

The smart treasury teams aren’t just hedging individual currencies. They’re asking: what happens if tariffs go to 15% while the dollar drops another 5%? What if the Fed signals no cuts until 2027?

These aren’t paranoid scenarios. They’re the current trajectory.

What to do this week

If you’re running finance at a company with real cross-border spend, here’s the short list:

-

Map your FX exposure by currency pair. Not just your top-line revenue split. Your actual payables, receivables, and intercompany flows by currency. Most companies have never done this exercise cleanly.

-

Calculate your tariff exposure. Which of your imports fall under the Section 122 tariff? What’s the annualized cost? How does that change if tariffs go to 15%?

-

Model the combined scenario. Take your FX exposure + tariff cost + current rates and project Q2 margins. Compare to your board forecast. If the gap is more than 2 points, you need to act now.

-

Talk to your bank about hedging options. Forward contracts, options, or even simple natural hedges (matching currency revenues to currency costs) can reduce exposure. The worst time to start hedging is after the move has already happened.

-

Watch the Fed announcement on March 19. If the Fed signals prolonged holds, the dollar could weaken further. If they surprise hawkish on inflation, it moves the other way. Either way, the volatility window is open.

This isn’t a one-quarter problem. Trade policy is shifting weekly. Currency markets are repricing geopolitical risk faster than most finance teams can update a spreadsheet. The companies that build real treasury infrastructure will protect their margins. Everyone else will keep finding seven-figure surprises in the quarterly close.

This is exactly the problem we’re building TreasuryPath to solve. Want to model your own exposure? Reach out.

The views expressed here are based on publicly available market data as of March 16, 2026. This is not financial advice. Companies should consult their treasury advisors and banking partners for hedging strategies appropriate to their specific exposure.