Payments Were Never the Point

You pay your providers in days and collect from your clients in weeks. For the weeks in between, you are the bank. Nobody set out to run a lending operation. It just grew inside the business, one payout cycle at a time.

Jeff Forkan · CEO & Co-Founder at TreasuryPath

July 9, 2026

Here is a shape I see in almost every services marketplace I talk to.

You pay your providers fast, because fast payouts are how you keep the good ones. The work gets done, the report clears, and money goes out the door in a few days.

You collect from your clients slow, because your clients are businesses, and businesses pay on net 30. Or net 45. Or whenever the invoice finally works its way through their AP queue.

So for the three or four weeks in between, the money going out has already left and the money coming in has not arrived. You are covering the gap out of your own balance. You are, functionally, the bank.

Nobody decided to start a lending operation. It just showed up inside the business, one payout cycle at a time.

Payments were never the point

Here is the part that makes it maddening. Payments were never the point of your business.

You built a marketplace. A place where the right buyer finds the right provider and the work actually gets done. That is the product. That is what your engineers should be building and what your customers are paying for.

Moving the money is a by-product. A necessary one, but a by-product. And like most by-products, it grew in the dark. First a card processor. Then a payout tool. Then a second bank account for reserves. Then a spreadsheet to tie it all together, owned by whoever was unlucky enough to be good at spreadsheets.

You are never going to build real infrastructure for this, and you are right not to. It is not core, it does not set you apart, and it does not drive growth. Every engineer you put on payment plumbing is an engineer not building the thing your customers came for.

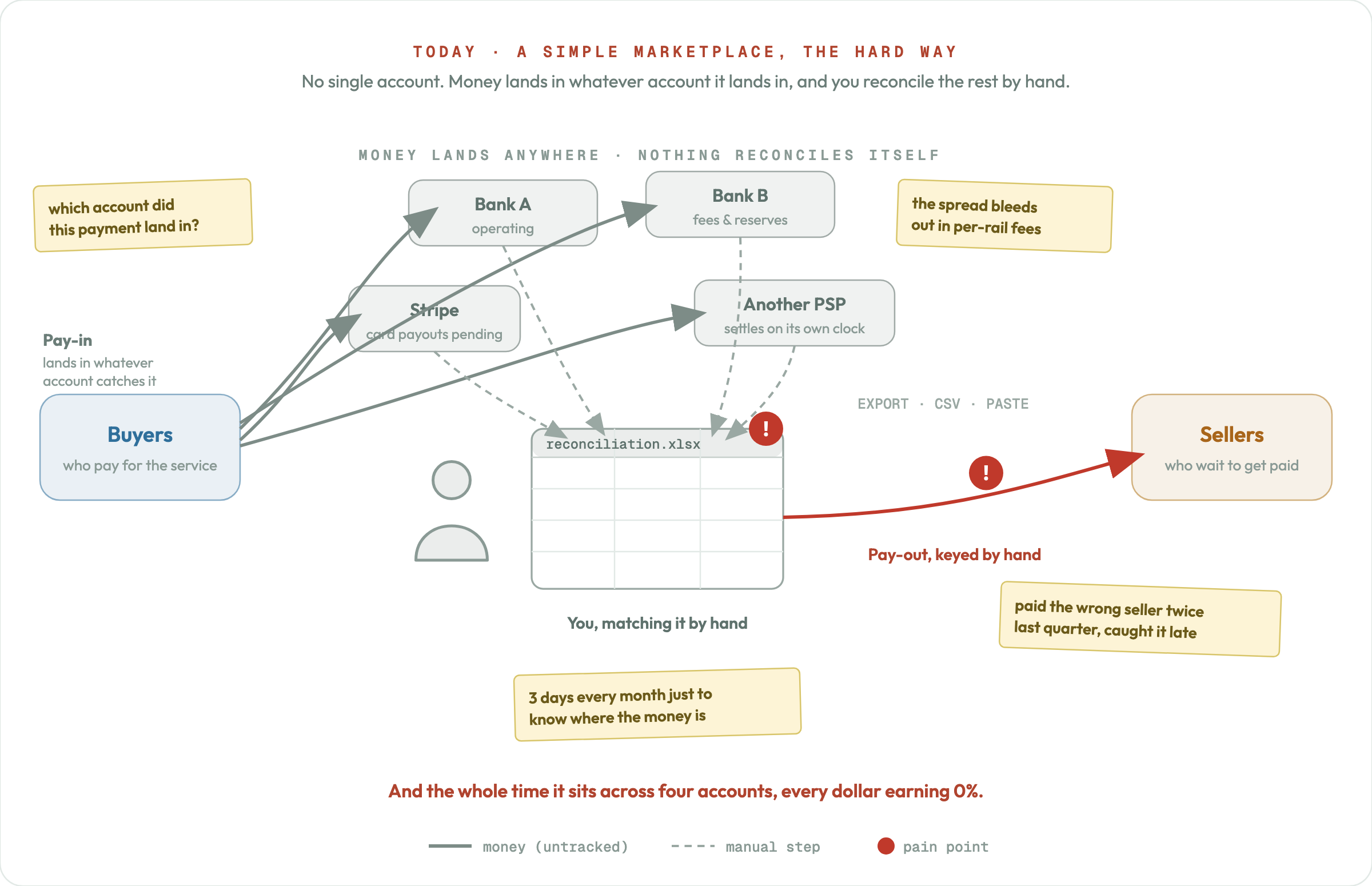

What it actually looks like today

A buyer pays. They pay however they want: card, ACH, a wire for the big ones. The money lands in whatever account catches it, on whatever timeline that rail happens to run. Now multiply that by hundreds of buyers a month.

Someone has to turn that into answers. Who paid? Against which invoice? What is still outstanding? That answer does not live anywhere, so it gets built by hand, by exporting statements and matching rows until the totals agree. Then the payouts go out, keyed from that same sheet.

And underneath all of it is the number nobody can see in real time: how much are we fronting right now? On a platform moving a few million dollars a month and collecting weeks later, the answer is often more than a million dollars, permanently. A real share of your last raise, tied up not in growth but in float.

For three weeks out of every four, you are the bank. Nobody signed up for that.

Your bank will not fix this, and neither will a TMS

The obvious question is why nobody has solved this for you already. Two reasons.

Your bank gives you accounts, not answers. It will hold the money and move it when you tell it to. It will not reconcile your pay-ins, connect to your billing system, or tell you what you are fronting this week. That was never what a bank was for.

And treasury management systems, the software built for exactly this, were built for the Fortune 500 treasury department. Six-figure contracts, six-month implementations, and a treasury team to run them. They are not built for a growth-stage marketplace, and to be honest they are not interested in one.

Too big for the money to manage itself. Too small for anyone to bother solving it.

That gap in the middle is where the spreadsheet lives. It is the reason we built TreasuryPath.

The layer that sits on top

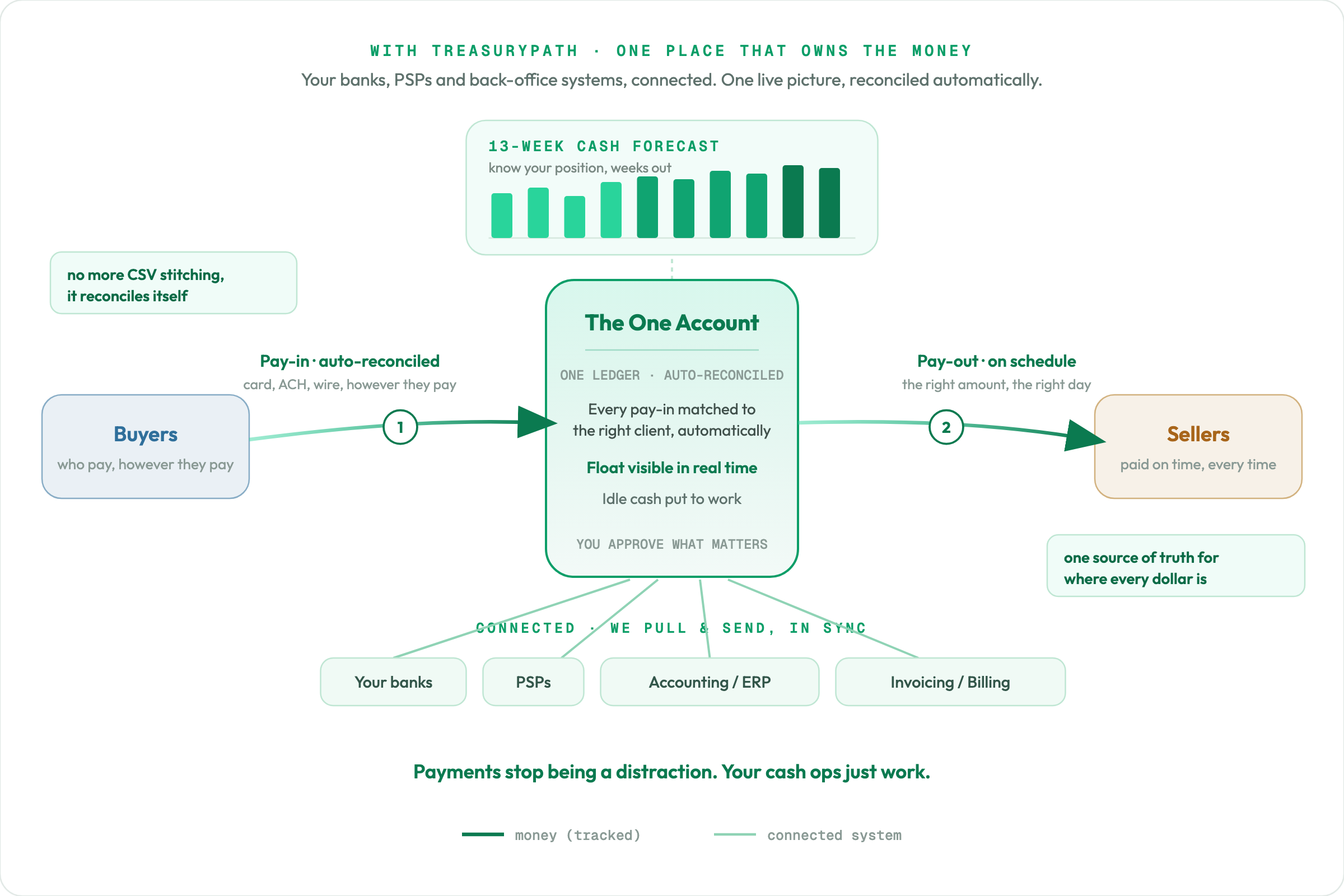

We are not a new bank, and we are not asking you to rip out what already works. Keep your bank. Keep your card processor. Keep the payout tool your providers already know and trust. TreasuryPath sits above all of it.

We connect the pieces you already have: your banks, your PSPs, your accounting or ERP, your invoicing and billing. Then we do the two things none of them do on their own.

We reconcile the money automatically. Every pay-in matched to the right client and the right invoice, no matter how they paid. The spreadsheet goes away.

And we give you a rolling cash forecast, tuned to how your clients actually pay rather than how the invoice says they will. So you can see the float coming before it lands, shrink the gap on purpose, and free the working capital that is trapped in it today.

What it looks like with one account on top

Same business. Same bank, same providers, same buyers paying however they like. The difference is that now there is one place that owns the money.

Pay-ins reconcile themselves. The float is visible in real time, per client, per day. Idle cash goes to work instead of sitting across four accounts earning nothing. And the forecast tells you where your cash is headed, so cash operations stops being a monthly fire drill and starts being something you feel good about.

You are not going to become a payments company. You should not want to. But you also should not have to choose between running the money by hand and hiring a treasury team you do not need.

Payments were never the point. They do not have to be the distraction either.

Jeff Forkan · CEO & Co-Founder at TreasuryPath

Fintech expert with 10+ years in sales and product leadership. Built Gusto's cross-border payroll from $0 to $20M ARR. Previously Head of Fintech at RemoteTeam (acquired by Gusto).

See it for your platform

Want your own money map?

We'll draw how money and data actually move through your business, and where they leak time and cash. No pitch, just the picture.

Book a working session